Thoughts On Digital Fiat Currencies From An Accountant’s Perspective

Friday, 10 May 2019By Robin Darbyshire

Introduction

As an accountant specialising in central banks, I take an interest in developments that might have an impact on central bank balance sheets. The creation of a central bank digital currency (CBDC) is such an item and this article contains some thoughts from an accountant’s perspective, as against those of the economists, technologists, and others who have commented on this topic.

This article does not attempt to reach any conclusions but, I hope, will add to the debate.

Reasons For A Discussion Of The Need For A CBDC

There are two main reasons for the discussion of a CBDC. The first is that payments are increasingly being made via electronic means, as against banknotes. This varies from country to country and between generations. The money used for such transactions is generally held in private institutions, such as banks or e-money services. Such money is backed by the assets of the bank or other issuer, and so is potentially at risk of a bank failure. In contrast, banknotes are issued by the central bank and hence backed by the assets of the central bank. A CBDC would provide a risk-free alternative asset to people to hold. Currently, the only such asset generally available is banknotes.

The second reason is the rise of cryptocurrencies, of which Bitcoin is the best known, and concern that these might replace ‘real’ money and pose a risk to monetary policy and perhaps financial stability. Commentators from this perspective generally think of a CBDC as a form of ‘official’ cryptocurrency with some of the same properties or features and using the same or similar technology.

These two reasons are not incompatible, in my view, but do create some areas which need addressing.

Nature Of A CBDC

The first area is the nature of a CBDC. In reading a selection of material, from both central banks and other sources, there seems to be a lack of consistency as to the nature of a central bank backed digital currency. Is it a separate currency or an existing currency in a different form? This confusion is compounded by the two main uses of the term ‘currency’ in English. Probably the most common usage of the term is in relation to the various national currencies used in countries around the world, such as US Dollars, Euro, Albanian Lek or Tajik Somoni. These currencies may exist in various forms, such as banknotes or bank deposits. Such currencies are bought and sold in foreign exchange markets with a price, or a range of prices normally known as an exchange rate.

The term currency is also used to mean the banknotes used in the jurisdiction denominated in the currency and which form the main visible form of the currency used by people in retail transactions.

Central bankers use the terms with both meanings. They may use the term currency management for the function that runs the note circulation. They also use the term in its wider meaning when discussing their policy on the exchange and foreign currency reserves.

The discussions on this issue seem to mix the two different meanings and sometimes equate currency with money, in a similar way to how the man in the street often uses money as a synonym for banknotes.

The usage seems to depend on the direction people are approaching the subject from. People coming from a payments and/or a retail usage perspective, including central banks, such as the Riksbank paper on e-krona, tend to regard CBDC as a kind of digital banknote or a deposit. In contrast, others, including those from a policy or economic background both inside and outside central banks, tend to regard CBDC as the wider form of currency, without full convertibility with the national currency, and with an exchange rate/price to the national currency. An example of this usage is the proposition that a digital currency can be used for international payments

The existing digital cryptocurrencies, such as Bitcoin, are not, in my view, separate full currencies, but have some features in common with them. They also only exist in one form, that used in the system, and the units need to be purchased. These cryptocurrencies do not involve any national authority so are not backed by anyone. Simply adding some form of government or central bank endorsement/guarantee might not seem to change the fundamental nature but, I believe it does, if only in the mind of the potential users. The acceptance by the authorities of a formal liability for the CBDC also importantly changes the nature from what is essentially a commodity, into a legal claim on somebody. As this claim is on the central bank, it makes the CBDC similar to banknotes or to a deposit at the central bank.

The issue of a CBDC as a form of digital banknote, or as an account-based arrangement, is an extension of the existing central bank money and does not cause any major conceptual issues, though there will be some legal and practical matters to resolve. However, a CBDC which is more limited in use and convertibility is more like a separate currency. Whilst it is probably possible for a central bank to issue two separate currencies, with an exchange rate between them, I find the concept rather difficult to comprehend in practice. In reality, the digital currency would surely be a denomination of the main national currency.

A further distinguishing factor is the manner of convertibility. A CBDC that is an extension of existing currency is readily convertible into another form of the same currency, just like withdrawing bank notes from an ATM, or paying them into your bank account. In contrast a digital currency that is akin to a separate currency requires somebody to act as market-maker, matching sellers with buyers and so ensuring liquidity in the market.

This is not just a semantic discussion; it also affects the recognition of the CBDC as assets and liabilities by banks and other entities. There are differing rules whether the items are money, securities or other types of assets. The accounting standards setters are working on how to account for the existing cryptocurrencies and have recently issued an opinion that a cryptocurrency is not a financial instrument. The accounting treatment will impact on the use made by businesses of the digital currency and or their willingness to transact in it. If the digital currency is classified as a cash equivalent it is more likely to be used in transactions, than if it is regarded as a commodity or other form of asset.

Holders Of CBDC And The Form Of A CBDC

A second issue under discussion is the potential range of holders of a CBDC. There seems to be a range of possibilities ranging from just banks, through other financial institutions, to the wider public. At the narrow end of the range, the use of the CBDC would be similar to the existing use of central bank settlement arrangements, though with wider participation and 24-hour operation. At the other end of the range, individuals would be able to access a CBDC. This makes the CBDC more akin to the existing form of central bank money available to the public, i.e. banknotes. An alternative explored by various central banks is that it could be regarded as a deposit with the CB. The terms that are being used are value based, for the digital banknote or account based for the situation where all holders have an account with the central bank.

The extent of usage brings a number of practical points, a major one being whether it is necessary for the central bank to have a record of the holders of their digital currency at all times and to be able to track the transactions. For a small number of users, this is practicable. However, if the usage is extended to the public this becomes more difficult. It would require capturing every single transaction in real time. Even if the volume of transactions is only a fraction of those using banknotes and other payment systems, there is a major technical issue to overcome. The tracking of transactions also raises issues of anonymity, which exists currently with banknotes. It is not essential to the usage of the CBDC to have such recording. Banknotes are not recorded individually. The central bank only knows the aggregate amount in circulation (and even this is not known exactly). So, a CBDC could operate in the same way. The key point would be to ensure that the digital currency could not be counterfeited, and that each unit can only be used once by each holder, so that users and the CB would know that the currency is genuine and will be accepted by others, including redemption by the CB.

What may require clarification, at least by the users, is certainty of transfer of title on the funds. For banknotes, this is currently by physical possession. The handing over of the banknote is the transfer of title. In contrast, many electronic transfer mechanisms may achieve certainty of transfer for the recipient but, may also result in a holder being overdrawn on their account if the user has made too many payments. A CBDC holder cannot overdraw his account at the CB, so some additional procedure has to be built in to prevent this happening.

Whatever the range of users, the CBDC needs to be issued in return for some form of funds paid to the central bank. If the range of users is limited, it may be practical for the users to transact directly with the central bank, however, if the general public are to be the holders, it is probable that mechanisms similar to those for banknotes may be required. These could involve banks, and other large users, buying the notes from the CB and then issuing these to their customers.

The reference to redemption by the CB raises another issue, the volume of the CBDC in circulation. The existing forms of central bank money, both banknotes, and commercial deposits, vary in aggregate from day to day and indeed throughout the day. For example, banknotes are withdrawn early in the business day and are repaid at the end of the day. The note circulation also tends to increase at certain times of the year, typically holidays. Although the central bank can set operating limits for the range, the ultimate determinant is the public demand. It can be expected that some of these aspects will pass on to a CBDC. For the CBDC to command acceptance the CB cannot refuse to redeem CBDC though it can set limits for operational purposes.

Impact On The Finances Of The Central Bank

(a) Balance sheet

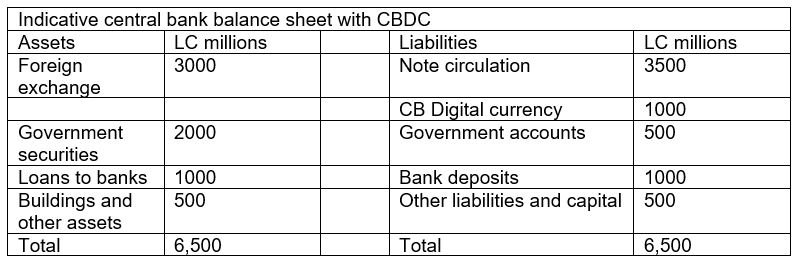

The issue of a CBDC will result in a liability appearing on the central bank balance sheet. This is one feature that distinguishes a CB currency from some other digital currencies, as there is a clear counterparty. In a similar vein the money created by commercial banks, (the majority of the money supply) is accepted as a liability by commercial banks. Central bank issued money is backed by the assets of the CB. This is specific in the case of the Bank of England notes which are backed by government securities in a separate accounting entity1. For most central banks, the bank notes and other CB money is not backed by specific assets but by the general pot of the CB’s asset portfolio, which may include foreign exchange assets, government securities, and loans to the government and to banks. For money issued by commercial banks, the backing is the assets of the commercial bank. There is not normally a specific allocation of a portfolio of assets to match the money issued, but regulatory requirements specify the proportions of liquid assets that a bank must hold. This achieves a similar purpose in ensuring that there are liquid assets that can be sold to match movements in the bank issued money.

It can be expected that a CBDC will be similarly backed by the assets of the central bank. This could be a specific portfolio, such as government securities, or the general portfolio of assets held by the bank. The issue of the CBDC will probably result in an increase in the size of the CB balance sheet, depending on the extent to which the CBDC replaces banknotes. The CB will, therefore, need to acquire additional assets. This may be government securities if these exist in sufficient numbers. However, in many jurisdictions, there will be insufficient of these available so the CB will need to take additional riskier assets onto its balance sheet.

(b) Income for the central bank

The issue of banknotes acts as an interest-free source of funds for central banks, which can then invest these funds in income-generating assets to provide revenue. For many central banks this income, known as seigniorage2, is a major source of revenue for the central bank from which it can pay its expenses. The low level of interest rates in recent years has caused financial issues for many central banks.

Any reduction in the note circulation, including as a consequence of replacement by digital money, will reduce the central bank’s income. Issuance of a CBDC will provide an additional source of funds which the central bank can invest for a return and so provide an additional form of seigniorage. However, if the CBDC is interest bearing this will reduce the net revenue.

Asset Backing For Money

This concept that money is backed by assets is an important factor, generally understood by central bankers but perhaps less so by other commentators. There are various theories on the history and basis of money. I am not going to comment on these as it is outside my area of expertise but will only say that the great majority of money is recognised as a liability by the central bank, commercial bank or other creator of the money3. The effect of this is that money, an asset from the holder’s perspective, is a liability of someone else. It also means that, as balance sheets must balance, there will normally be assets backing the liability. Whether or not this is essential for something to be used as money, it is a reality and must aid the convertibility of between the differing forms of money. For example, banks will readily accept banknotes paid in by customers for credit to their accounts, because in the end, they know that they can take them to the central bank and get value. This, in fact, happens as notes move between the commercial banks and the central bank every day.

Ultimately, it is the user who determines what they will use as money. People will only accept something in payment if they are confident that they can also use it themselves. In practice, this means that most banknotes are only readily useable in their own jurisdiction. In some countries, there is little confidence in their own currencies and so people use another form of payment. In practice, this is someone else’s currency, most commonly US dollars or euro.

(a) Central bank backing for banknotes

Central banks recognise the notes in circulation as a liability and there will be assets on the other side to match these. Some central bank laws require the note circulation to be

backed by assets such as the foreign currency reserves and/or gold, and they may have limits on the amounts of notes that can be issued in excess of any specific portfolio of assets. For example, the Bank of England has a separate accounting entity, the Issue Department, which records the notes as a liability and has a dedicated portfolio of assets to match them. This is unusual in being so specific but the concept of assets backing the notes exists in central banks generally even if they are not separately identified.

Central banks may use the term Fiduciary Issue, for the number of notes issued without the specific backing of gold/foreign reserves, as it reflects the fact that the issue is based on faith or trust. Central banks manage the daily movements in the note circulation, arising from public demand, through adjustments with other assets or liabilities. Movements in the note circulation typically have a counterpart in the commercial banks’ balances with the CB.

This backing of the notes with assets acts as a support for public confidence in the money and provides some resources to meet the movements in the amount of currency required by the public, without the need to call on the government. Although the general public may not be aware of the details, they do believe the notes will be honoured by any bank and by the central bank in particular.

(b) Commercial bank backing for money

The majority of money exists in the form of deposits or other claims on commercial banks. These form part of the bank’s deposit base which will be matched by assets of varying types and maturities. Commercial banks will not have a dedicated portfolio of assets matching these deposits, but regulatory requirements govern the amount and form of assets held by banks. These will include very liquid items that can be realised quickly to meet outflows of deposits. Commercial banks manage their balance sheets and amongst the factors considered will be movements in deposits.

Impact Of The Existence Of A CBDC

The use of a CBDC may have consequential effects on the use of other forms of money, in particular, banknotes and bank deposits. Bank deposits as the largest component of money, form the basis for making many payments through the various clearing systems. It is unlikely that the CBDC can replace bank deposits in their entirety, despite some commentators’ dislike of money created by commercial banks. As described above, the central bank issued currency requires backing by assets. If the currency issued by the central bank increased to replace other money, the backing asset would be a government security. The magnitude of such a security would be very significant for public finances. In simple terms, the state would need to issue a liability to cover money currently backed by commercial bank assets. Some commentators may say that this reflects the present situation where the state is responsible for all the money. But currently most of this is merely a contingent liability, only required if a commercial bank fails, and cannot meet its claims out of its own assets. Making all money a liability of the central bank with the matching security crystallises the claim.

At this point, it might be worth reminding people how commercial banks create money. The creation takes place when a bank makes a loan or overdraft. The position is most easily explained in a form of double entry. The entries for the creation of the loan are

- Debit - Loan

- Credit - Customer's current account.

The balances that now exist on the customer’s account can then be paid to others at the customer’s instruction and thus are used as money. Payment, or withdrawal in banknotes, is a transfer of money from one person to another, or from one form to another. It does not create the money. Having granted the loan and created the deposit, the bank must rearrange its balance sheet to ensure that its own liquidity and other assets, meet its own, and importantly the regulators’, requirements.

In addition to any prudential requirements, central banks have other tools for restricting commercial banks’ ability to create money, such as reserve requirements, under which banks are required to deposit a percentage of their deposits at the central banks. These requirements vary from country to country, and from time to time. Some countries pay interest on them, others don’t. Some countries require reserve deposits in both foreign currency as well as the domestic currency.

Notes

[1] This does not apply to other forms of central bank money from the Bank of England, which are backed by the general assets of the Bank.

[2] This definition of seigniorage, the income on the assets matching the note issue, less the expenses incurred in the issuance of notes, is used by central banks. The alternative definition, being the face value of the notes less the costs of production, is not used by central banks for notes. It may be used by governments for the issue of coins.

[3] The only exception is coins, issued by governments, who may not treat them as a liability.

Further Reading

Bank of England Staff Working Paper No. 725 Central bank digital currencies — design principles and balance sheet implications

Sverige Riksbank. the-riksbanks-e-krona-project-report-2.pdf

Bank of Japan Working paper wp19e02. Digital Innovation, Data Revolution and Central Bank Digital Currency