Of Purpose & Allocation: Betting Against ‘MAGA’ Is Risky But Then So Is Britain’s Recovery

Monday, 31 August 2020By 'JB' Beckett

When investing on an agenda of purpose, and diversification, have U.K. asset allocators unwittingly put the global economy before the interests of the British economy. Possibly.

To my fellow Investment Committees and Boards,

In more recent years U.K. insurance companies, pension schemes, centralised propositions, charities and asset managers have increased their weightings dramatically to overseas markets by around 20-50% (out of a total 100% allocation) from what I have seen first hand. We may soon see U.K. assets make up little more than 20% in some strategies. What we have seen is a philosophical and physical (cash) exodus out of the U.K. Actuarial models continue to calibrate increased allocations to reflect the dominance of world growth over the last 20 years. What were once only ‘footsie’ names, in pensions and portfolios, are now invested across a smorgasbord of bourses in United States, Europe, Asian Dragons, Pacific Tigers, Emerging Markets and Frontiers. Once wholly U.K. Gilt portfolios are now invested in overseas corporate bonds and Global High Yield. Only property allocations have remained U.K.-centric but recent liquidity challenges to open-ended funds and a dimming view post covid-19, and generally, towards Britain’s high streets and offices may reverse that.

You will recall the old investment thesis for overseas investment was simply to gear-up each pound by investing into countries and sectors with higher growth rates that both maximises Return of Capital (ROC) and supposedly offers diversification to investing only into the U.K. economy. I, like many of you were, was sold on the elegant merits of overseas diversification. This global shift has reduced the domestic investment in British companies. Today U.K. investors own less than half of U.K. FTSE350 companies;

“Orient reveals that 35.9% of shares in UK companies in the FTSE 350 are owned by funds and trusts operated by North American companies, with passive fund managers such as Vanguard and BlackRock dominant. ‘Since the EU referendum, though many foreign investment managers shunned UK companies, there was a remarkable acceleration in interest from those in North America, who almost doubled their stakes in the market, from owning 19.8% to 35.9% at the end of May this year,’ In investment terms, the tectonic plates are shifting beneath us and ownership of the UK market is being pulled across the Atlantic‘ the report states.”

I look over the Atlantic to America, which appears to be holding all the cards from an investment point of view. A protective trade policy that favours domestically purchased goods, the global reserve currency of the world, the largest investment and stock markets, the largest debt markets in the world, the largest banks in the world, the largest asset managers in the world, servicing and data services, depositories and a dominant Big Tech industry that fuels supersized exports, growth and capitalisation. Apple just became the first $2 trillion company, or the total value of a medium sized European country. California GDP is worth around $3.2 trillion, much more than the U.K., about the same as Brazil’s GDP. Even the rules, tools and conventions of asset allocation are now largely US-centric and globalised by the likes of the Chartered Financial Analysts Institute (CFA).

US Equities now regularly feature more than 50% of market-cap-weighted global baskets. Many U.K. allocations allow only limited tracking errors from global benchmarks. Many actuarial models are also now predisposed to assume a US allocation. This baselines a model to ensure a high global allocation is now virtually guaranteed. It is worth noting that actuarial consulting, asset management and index provision are all dominated by US firms today. It is hard to now build an asset allocation that is not heavily weighted in US assets to the point ‘Global’ has almost become shorthand for US. Trump famously used a Reagan-redux campaign of ‘Make America Great Again’ and ‘Murica’ First’ and to great effect. Okay not great but you know what I mean.

The same has been true of allocating to Global Emerging Markets. Whilst allocations have typically been smaller; they continue to be calibrated as higher beta engines of growth. Again much of the calibration in GEM has been supported by China’s 20 year expansion, Hong Kong, and surrounding Tiger economies. Lastly global allocations are also rising through investment into ESG-tilted Exchange Traded Funds. Together they combine to squeeze traditional allocations into the U.K.

Many Strategic Asset Allocations, today, are the result of calibrated Actuarial Models, which are moving to long-run global biases.

Consider that many committees traditionally started from a base position of 100% UK Equities. To this they would seek supplementary exposure substituting UK Equities with Overseas Equities to provide further diversification and access to opportunities not available in the UK. There has been a sea-change to move the base position to 50-100% global and then modelling a smaller U.K. position back in. There are a variety of reasons why this is happening. Some observations;

- The guiding philosophy of accumulation and income strategies might diverge on assumptions, at some point, reflecting the different demands of growth versus sustainable income, the needs of customers therein and with a knock-on effect to the SAA optimisation, and TAA.

- Many large pension strategies effectively operates as a ‘supertankerfund’ using building block strategies (‘sleeves’) that can prove quite an obtuse toolset for both SAA and TAA implementation. Growing size can make the fund (operationally and for idea generation) unwieldy.

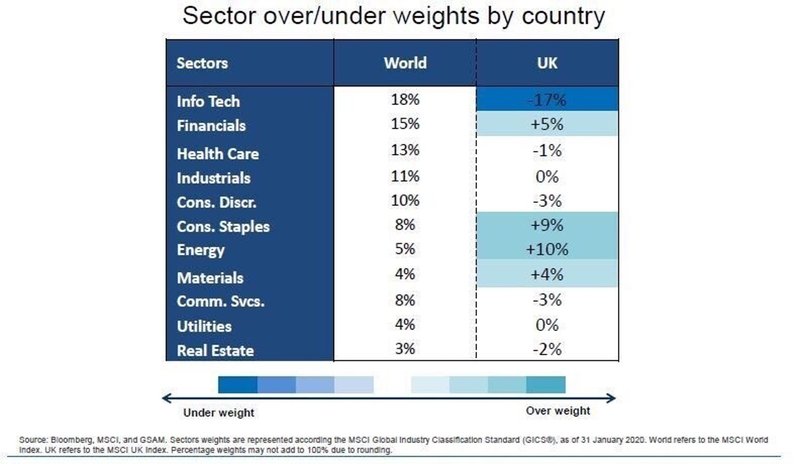

- The U.K. economy suffers three significant skews compared to US markets; an underweight to Big Tech, Banking largely devoid of investment banking, and overweight to E&P and Commodity extractors. The U.K. does have exposure to Pharma/Biotech but is at risk of falling behind leaders US, China and EU. I expect the rising agenda of pandemics will be a dominate theme for a period extended beyond the current COVID-19 crisis. Likewise the competitiveness of the City is cast in doubt post BREXIT.

- The rest of the world (ROW v U.K.) debate tends to skirt over the reality. Any bet on U.K. is a bet against US and China. US dominates world equity baskets; China is the manufacturing room of the world and both countries dominate Tech and Pharmaceutical. If we see US and China as continued leaders of capital markets and world economy them we should critique the UK’s outlook versus US and China. Here we have to also unpick certain markets for the very largest stocks in order to get a good read on valuation (eg. S&P top 10 versus 500) and multiple expansion and stretch (between top and bottom of the index) within.

- Country error: we should thus look at our UK portfolio and model as two distinct portfolios; firstly large multi-nationals that derive majority of earnings overseas and thus leveraged to the world economy and profits (looking at assets by economic exposure tends to be better than by listing), distinct from companies that are ostensibly domestically U.K. focussed. The fact these companies might be listed in the U.K. is where the similarity ends. Hence looking at from an economic factor perspective helps. Here currency effect also comes into play.

- There are two conflicting pressures then on the SAA: meeting near term returns and facing off to trends like Moore’s: FANNGS as well as decarbonising versus longer-term the purpose of capital deployed in U.K. and investing in U.K. transition, jobs, earnings, tax receipts and rising political and public pressure etc.

- The portfolios are then doubly impacted through property exposure, which is a second order effect of the competitiveness of the U.K. economy. It is effected by office occupancy, Retail profitability, manufacturing and distribution. Thus we cannot always assume the property portfolio is a diversifier in the long run to a U.K. overweight allocation. U.K. property exposure tends to be U.K. only.

- Lastly we should thus consider if the a given model and starting assumptions (eg. 50:50 mix) represent model risk and thus right we challenge? Model and assumptions error can be prevalent. I refer you to John Kay’s recent article on this; https://www.johnkay.com/2020/07/24/michael-gove-john-von-neumann-and-the-reverend-thomas-bayes/

The Economic Effects of U.K. Divestment

What of the U.K.? Hanging on by its fingertips to stay in the G10, the U.K. is facing some very tough choices ahead. It was reported by OECD that the British economy was the worst hit among major economies from April to June, with a 20.4% contraction almost double that of the G7 average. The 9.8% drop in GDP for the 37 major economies in the OECD area was the largest on record, a fall four times as large as that seen during the height of the financial crisis in 2009.

Comparably, the eurozone saw a drop of 12.1% and Germany's GDP shrank by 9.7% over the same period. Investing in non U.K. companies may seem an obvious way to diversify a U.K. recession.

Yet investing in British companies doesn’t have to come at a cost to diversification if we use the correct tools.

Consider the London Stock Exchange (LSE) has in the last 30 years become a global exchange for companies exporting heavily into the world economy. Indeed investing in British asset managers with global footprints offers one option; perhaps blended with U.K. managers investing in UK assets. More widely, typical estimates of around 50% of the earnings from the FTSE250 come from overseas, and as much as 75% from FTSE 100 firms. Therefore it is perfectly possible to invest in the global economy through British domiciled companies, which ensures earnings and tax flow back to the U.K.

Secondly the LSE is a means to invest in non British companies. Non British companies bring in new breadth, scale and liquidity. Indeed the LSE now boasts its international exposure;

“London Stock Exchange welcomed over three times more international companies to list on its markets than any other European exchange in 2018. Three out of the five largest IPOs in London in 2018 were from international companies. AIM continues to be the leading international growth market, helping companies raise £5.5 billion in new and further issues during the course of 2018.” https://www.londonstockexchange.com/news-article/LSE/annual-financial-report/13986365?lang=en

This gives rise to two distinct U.K. economies; domestic and overseas. I contend that these need to be modelled distinctly, as current models are underestimating inherent global exposure through U.K. assets. When then increasing global allocations it will likely lead to an overshoot in country and economic factor terms.

In doing so committees can appraise the global exposure they receive through British companies; versus those companies/assets that are wholly hinged on domestic consumers and purchases. Separating out these economies helps address the industry sector skew of the U.K. versus ROW.

As one Actuary noted to me; “We should be acutely aware of the rise of thematic investment and the impact that might have on capital flows and therefore on this decision. How much difference should we expect to see between a market cap/sector benchmarked ESG integrated global portfolio and a climate change risk thematic portfolio for example. What do we believe about expected returns and risk? This leads me to having some sympathy with the suggestion we should be playing to the strengths we have in XXXX, providing we have enough business tolerance for the potential consequences of a high tracking error against the market cap benchmark and the competition.

The second is that I am somewhat sympathetic to the argument that our retirees will retire into the UK economy and thus additional exposure to that economy (as distinct from a U.K. listing - a point you also note) seems reasonable. I wonder to what extent this argument might be amplified by our thinking about purpose? As a U.K. mutual, I think our notions of purpose are likely to be and should be limited to purpose that is of relevance to U.K. customers (doesn't just mean UK geography necessarily, but this will surely dominate?). If so, then again there may well be a further justification for an overweight to certain aspects of the UK economy - those that will impact customers in retirement - good social housing, good social care etc.” Anon.

What then can UK investment committees and investors do to support Britain’s recovery? It sounds obtuse but simply put; ‘buy British, and invest with and in British companies’.

The last few months has been very painful for the U.K. economy. The OECD has noted that the U.K. was hardest hit among the largest developed economies. All eyes are now on recovery, by what means we will recover and what sort of economy we will recover to. What role will U.K. asset management play? Writing in the Daily Mail, Bank of England’s stoic Mr Haldane said the economy is expected to expand by more than a fifth in the second half of the year, which would be ‘by far the fastest rise’ since quarterly records began. He says: “The foundations for an economic recovery – a rapid one – are already in place, hiding in plain sight. Economic activity in the UK is not falling like stone, in fact it has now been rising for more than three months, sooner than anyone expected. It has also recovered far faster than anyone expected.”

The Investment Association is likewise keeping a brave face; “Investment management remains one of the UK’s global success stories, with assets under management standing at £7.7 trillion in 2018, in spite of a year of economic and political uncertainty as the UK prepares to leave the EU. This represents an increase of over 150% (£4.7tn) compared to a decade ago, according to the Investment Association’s (IA) Investment Management Survey, the largest annual study on the state of the industry.” September 2019. https://www.theia.org/media/press-releases/uk-investment-management-industry-retains-global-position-against-economic-and

Yet the stats from the Investment Association highlight a continued move out of U.K. funds into overseas funds. In June 2020 the U.K. All Companies sector saw -£662m redemptions, UK Equity Income lost -£327m and the U.K. Smaller Companies sector saw -£68m. With the All Companies still around £150bn then few will see the problem but the trend is growing across pension schemes and segregated mandates for Institutional investors too. For example if you do the sums, more equities are now being managed outside of the U.K. through IA funds, than inside. https://www.theia.org/industry-data/fund-statistics/statistics-by-sector

Meanwhile behind the City’s steel and glass, those activities and profits within are not necessarily pursuant to growth back into the U.K. economy, with the majority of investment firms now non-British. Today there are fewer home grown asset managers that have not been acquired by US or European conglomerates. Consolidation and M&A activity has accelerated post Great Financial Crisis. Aberdeen Standard, Schroders, Royal London, Legal and General and Baillie Gifford stand among the few genuinely large British brands that are still British controlled.

By far the majority of British asset fund managers are controlled and owned overseas including many of these hallowed names. U.K. asset management has been dominated by US firms since the ‘Big Bang’. Whether early entrants like Fidelity (surely the Ford of British asset management) or firms that have entered through acquisition; Blackrock, Columbia, Invesco, Legg Mason, Franklin Resources. The shift in British-controlled assets (proportionally) has been obfuscated by the overall rise in assets reported by the industry as a whole. This flow to overseas firms has also been symptomatic of the shift to index based products and Exchange Traded Funds.

I expect few investors will stop to consider where the earnings and profits of their investments go.

Be in no doubt when it goes to Blackrock, Threadneedle, Invesco, Franklin Templeton or Legg Mason then the answer is Stateside. Most U.K. subsidiaries of overseas multinationals will pay dividends back to their group corporate. This profits from U.K. investors are helping to fuel the American economy. This is not to overlook the huge positive effects for the U.K. economy. Asset management funds jobs, it grows pensions and generates tax revenues for the Treasury. I myself worked for an American asset manager for 6 years and it was a great employer. Is ‘buy British’ a buy note for U.K. boutiques? Beneath the headline AUM figures; there is a plethora and rich universe of British boutique asset managers to choose from.

Long-term Drivers of UK disinvestment

We can look at the prodigious buildings in the City and rightly admire London as one of the greatest capitals in the world. However it’s a City that hitherto hasn’t belonged to the U.K. for quite some time. It’s an economic island, operating its own form of sovereignty just as much the Vatican does from Italy. Most firms in those big buildings are not British. Investment Committees, the decision-makers of the City, have engaged in great asset rotations including; moving equity baskets overseas; bond allocations away from U.K. Gilts and increasing U.K. property exposure that in turn form the many towers in the City, buoyed by foreign investors. It is worth reflecting why;

Index primacy: The immutability of the market cap mechanism has fuelled increased global investment through index-tracking baskets. The sell is easy; diversify your country allocation, spread your earnings sources and allow the index mechanism to capture the winners, which are deemed unpredictable by the likes of Morningstar’s ‘patchwork’ charts and maps. https://www.morningstar.co.uk/uk/Markets/global-market-barometer.aspx

Moore’s Law: Industry rotation has been a key primer to address UK’s ailing global competitiveness and countries like America and China have captured huge market share in the new digital economy. FANNG stocks dominate the S&P500. https://uk.reuters.com/article/uk-usa-stocks-s-p500-graphic/big-tech-drives-sp-500-to-record-high-in-coronavirus-rally-idUKKCN25E2CY

Longevity: Big pharmaceuticals and Biotech are huge business even before the global COVID-19 pandemic. As we get older our expectation for life rises even as we get sicker with age. This has driven a huge race in diabetic, oncology and anti-viral drug production. https://medicalfuturist.com/5-things-that-will-dominate-the-2020s-for-pharma-companies/

GEM and BRIC: Jim O’Neil’s thesis in 2001 changed Asset Allocation for the next 20 years by sign-posting that Brazil, Russia, India and China (‘BRIC’) would ascend to become new world leaders. It has increased interest in emerging and frontier markets that encompass and satellite these new super powers. Globalisation itself has encouraged overseas investment, offshoring operations and access to new growing consumer markets. https://www.goldmansachs.com/insights/archive/archive-pdfs/build-better-brics.pdf

Diversification is king: The very concept of diversification traces to Roger Ibbotson’s and Gary Brinson’s 1990s studies that noted the majority of returns stem from asset allocation rather than asset selection. These encouraged increased diversification from the sensitivity to one asset class or country. https://blogs.cfainstitute.org/investor/2020/03/25/roger-g-ibbotson-what-works-in-asset-allocation/

Actuarial Models: Operating calibrations based on long-run returns the effects of a 30 year bond bubble, commodity super-cycle, 10-year US bull run versus a relatively flat U.K. market and staid Sterling bond market have all loaded up overseas allocations.

ESG: The increased purpose now working into the terms of many a Committee has a fairly broad narrative of changing the world for the better. Add growing revulsion to industries like Tobacco and mining extraction and the U.K. index is exposed. Investment to change other economies reflects a WASPish perspective of democratic and sustainable values. There is a clear overlap with the globalism. Most new ESG and climate investment have been through index tilted ETFs.

End of the U.K. Bond Bubble: a flight away from the nil rate bound and even negative Gilt yields has broadened into a race for Global High Yield (‘Credit’) and overseas bonds.

Brexit: Many investors are hedging their U.K. positions by investing overseas, in the event of a ‘hard exit’ from the EU, vociferous trade deals or threat of Scottish independence. Many argue that the current value of the U.K. market reflects these risks; others that the U.K. remains an undervalued opportunity and we have even increased investment from the US and overseas. https://www.gov.uk/government/news/overseas-investment-into-the-uk-at-highest-ever-level

U.K. Property, the great bond proxy: Property in London has become highly leveraged on London’s role as a capital centre and a flow of capital. One of the most rapid urbanised cities, commanding higher than global average rental yields and valuation inflation. It is highly levered to the global economy and foreign direct investment. https://www.worldpropertyjournal.com/real-estate-news/united-kingdom/london-real-estate-news/london-real-estate-news-coronavirus-impact-on-london-property-market-in-2020-knight-frank-london-property-data-for-2020-12068.php

Purpose: What can Boards and Committees do?

Buying U.K. funds managed by U.K. fund managers could become a new goal for investors. Domestic active and passive wfunds are accessible, even ESG, Impact and sustainable strategies are available. Consider, when increasing your overseas allocation, the context to their economic effect on the U.K. in its entirety rather than narrowly in terms of their portfolio risk-reward ratio. Should U.K. investment committees and Boards now consider both the origin of whom they are invested through, as well as where they are allocating to?

Committees must dutifully discharge their fiduciary duties by diversifying portfolios and managing risks but I suggest they should also expand their responsibility to consider purpose and benefit to U.K. economic exposure (earnings, wages, contribution to economy and tax);

- For investors; invest in U.K. headquartered asset managers, employing staff in the U.K. (versus offshoring). Consider the risk of feedback from U.K. disinvestment.

- For asset managers; invest in U.K. companies; discerning a mixture of overseas earners and domestic stories. This can include smaller companies, AIM listed, greening Finance, private listed and impact markets.

- For consultants and actuaries: critique models that apply one model for U.K. assets or economy. Challenge models that baseline a minimum global allocation. The U.K. is made up of different sleeves, and economies, with different economic exposures.

- For Board members; irrespective of whether your firm’s earnings flow offshore or stay in the U.K.; consider your fiduciary duties more broadly, consider how your are supporting the U.K. economy, workforce, capital investment, balance of trade and transition economy.

- Invest for purpose, absolutely, but purpose firstly linked to the society, social, environmental and economic welfare of the U.K. populous.

Compared to ‘Make America Great Again’; Britain sadly is not so Great but we can ‘Make U.K. Again’ a strong and purposeful economy. Boosting recovery, not by closing our economy, nor blocking investing overseas, but instead considering the full economic effects of our allocations.