Gaslighting Europe

Monday, 31 January 2022By Amit Sharma

Out of the Frying Pan

Its impossible to ignore the fact that we are living through an energy crisis, which is leading to a possible doubling of consumer electricity and gas prices for UK and many European consumers. The idea of this paper is not to go through the reason behind this, but rather the impact and possible consequences this could have on financing for corporates in the UK and further afield.

Moscow And Ukraine

The stand off currently occurring on the Russia/Ukraine border is a fluid situation, and politicians around the world are reviewing the weather to see when the Russian tanks may roll in- slightly warmer conditions this week, have left marshy conditions underfoot, suggesting an attack is not imminent.

But why does an event over a 1000 miles away from London matter to the economy and, in particular, the potential liquidity available to companies in the UK and Europe?

The primary reason is sanctions, and in particular US sanctions.

Since the Obama regime, these restrictions, the hard end of soft power, have become a fashionable and a low cost alternative to using military force. Currently there are over 7000 restrictions in place covering both countries and individuals.

The three key aspects of sanctions are

- trade barriers;

- tariffs and;

- restrictions on financial transactions.

It’s the third of these restrictions which poses the greatest risk of tripping up companies and their financial partners.

Why US Sanctions Matter So Much

This is not a legal review, and the analysis/interpretation can be quite complicated, but its important to understand why the Americans are so powerful and successful in imposing these restrictions. The key point here is that the US dollar’s status as the world’s dominant currency. International business, even outside of the US, is often traded using the greenback- think of commodities such as oil, gold, wheat, corn and soybeans.

The restrictions imposed by the US Government, not only apply to the recipient, such as Iran or North Korea, but also to any party trading with them, in particular banks. It suddenly makes it very difficult, in facts, nigh on impossible, for banks to interact with these countries or sanctioned entities contained within them. Those that do, and there are numerous instances of this (including BNP, Standard Chartered and HSBC ), not only face large fines for breaches, but they risk losing their ability to clear USD through New York.

Sanctions And Multilateralism

For sanction to be effective, its important that they are applied by as many countries as possible, and typically the US, UK and EU are aligned on their sanctions against states like North Korea. The regimes used to administer these regulations are different, the EU Council, UK Parliament and the US through OFAC (Office of Foreign Asset Control) and SDN (Specifically Designated Nationals).

EU and UK sanctions are not designed to have extra-territorial effect on players outside the EU, but the same cannot be said for the US, whose impact is much wider. It basically means that every company around the world that uses US dollars or has ties to the US must respect American sanctions or face the risk of falling under sanctions themselves. In a perfect world, all western countries would impose the same level and manner of sanctions and it would be possible for business to follow a single simple list, but we are far away from this and likely to get further.

Divergence

We already have situations where countries have different degrees of sanctions, for example on Iran, where the UK implemented the Financial Restrictions (Iran) Order, which went further than EU sanctions by prohibiting UK financial institutions from dealing with Iranian Banks. Furthermore, the ECJ (European Court of Justice) in December 2021 adopted a judgement blocking the impact of US extra-territorial sanctions on European entities – a so called ‘Blocking Statute’ – but this has yet to be tested in practice.

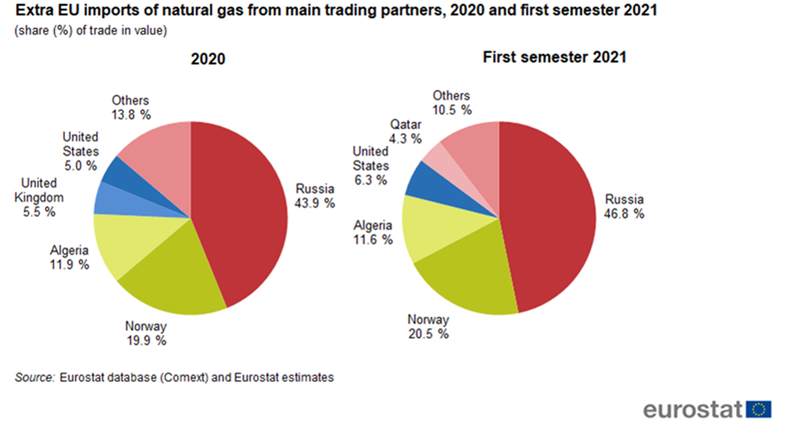

We can expect the real test on further divergence to come in respect of Russia. As we know, Europe is heavily reliant on Russian fossil fuels, with some states entirely dependent on Russian gas.

Since last year supply has been constrained and prices have risen considerably as we can see below, whilst Putin has been massing troops on the Ukraine border. Should Russia invade Ukraine, the Biden Administration has been very clear that it will impose strict and wide ranging sanctions. The question for Europe is whether it will follow suit and, if it does will it be willing to face an energy crisis that could be many times worse than what we are facing now, in the midst of winter.

Possible Impact

Its not hard to imagine a situation where the EU countries do not follow US sanctions and continue to trade with Russia and import large levels of gas to maintain its energy supply. For the business community its not only sanctions that are difficult to deal with, but rather the divergence between different regimes and the complication this can lead to.

In our inter connected world, divergence is likely to be an administrative nightmare, with companies and their banking partners having to dedicate huge amounts of time and resources to abiding by different sets of regulations. The knock on effect will of course be an increased cost in doing business and a possible drop in liquidity. Financial Institutions not based in the EU and in the US for example, could find it difficult to partner with non US entities and this can include banks, USPP and bond investors and even equity providers. For large International Companies, being locked out of the US market and the huge investor base could be very damaging

The above situation hopefully will not come to fruition, but its not outside the realms of possibility. In a multi polar world, where China is fast becoming the EU’s largest trade partner and Russia its energy supplier, continuing to support the Atlantic alliance will come at a considerable cost to EU citizens, in the midst of what could be a very cold winter.